Junior doesn't vote

One of the best political interviews I’ve seen in years is François Bayrou’s interview, the French PM, on the French evening news by Gilles Bouleau on Wednesday, 27 August 2025 8 p.m. news.

François Bayrou had just announced on August 25 that he would be seeking a vote of confidence in the National Assembly. The PM sought backing for €43 billion in budget cuts with a minority government. The package included freezing welfare, pensions, and tax brackets at 2025 levels, plus a proposal to scrap two public holidays. All of this against the fiscal backdrop of a 2024 deficit of 5.8% of GDP, the largest in the Euro area, and sluggish growth of 1.2%. At the time of the interview, Bayrou realized that he was headed for an almost certain defeat in the National Assembly and the end of his tenure as Prime Minister of the French Republic. The best part starts at minute 20, just as Bouleau was getting ready to wrap up the interview. Bouleau interrupts him a couple times to thank him for the interview, but Bayrou ignores him. He’s getting really worked up in spite of the fact that he looks visibly tired and haggard.

"And if we create chaos today, once again, who are going to be the victims? The first victims are the youngest French people — the ones we've managed to fool. As I said earlier, this will be in the history books: they're the victims, they're the ones who'll have to pay the debt their whole lives, and we've managed to convince them it should be raised even further. Don't you find that brilliant? All this for the comfort of certain political parties and for the comfort of the boomers, as they're called, who from that standpoint reckon that, well, everything's going just fine. I believe lucidity is a nation's first virtue, along with the will to pull through."

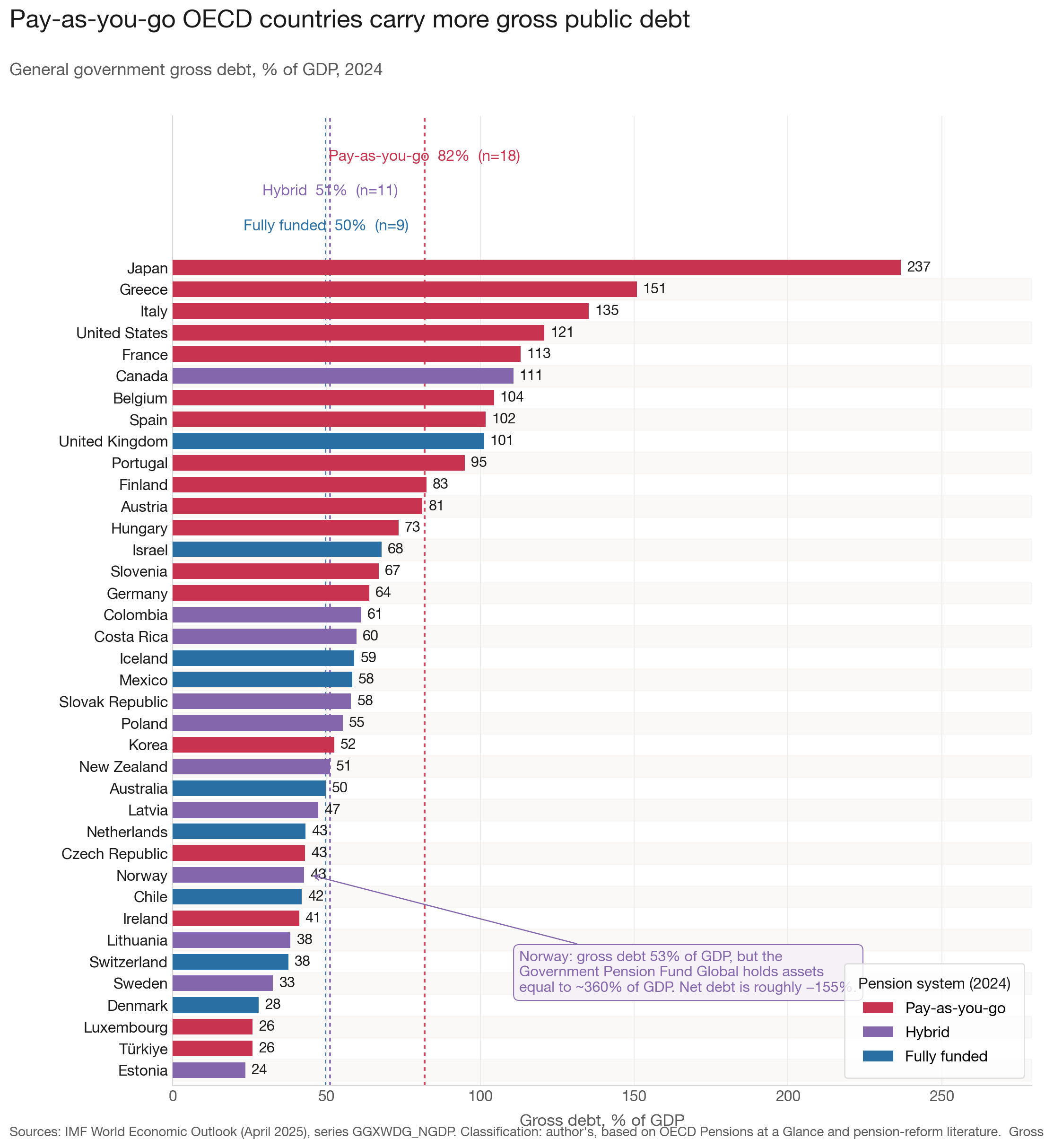

It’s so much better in French. “Vous trouvez pas ça génial ? “ Don’t you think it’s brilliant? “Tout ça pour le confort ...des boomers.” This was the first time I have ever heard a sitting head of government clearly articulate what these debates are really about: intergenerational transfers. In countries like France, with large pay-as-you-go pension systems, the boomer generation has promised itself large payouts. Governments in these countries are struggling to keep these promises. And in order to avoid tough choices and trade-offs, these governments have resorted to issuing more debt.

But pensions are only the part of the transfer you can see. The bigger one is quieter, and it doesn't run through the pension system at all — it runs through asset prices. For more than a decade, real interest rates were held near zero, and a low rate is just a high price for anything that pays off in the future: houses, stocks, long-dated bonds. The people who already own those assets are, overwhelmingly, the old; the people who still have to buy in are the young. So the same cheap money that let governments roll their debt also revalued the entire national balance sheet in favor of whoever already held it. A retiree watched her house and her portfolio climb year after year. Her grandson watched the price of the life she'd had — a house, a foothold — climb out of reach. Nobody voted for it. No reform passed, no budget line appeared, no minister went on television to defend it.

A rise in the price of an asset is a transfer from whoever was going to buy it to whoever already owns it — and when the holders are one generation and the buyers are the next, that is an intergenerational transfer, just one that never has to admit what it is. Which is what makes it the perfect transfer: it's invisible, and the invisibility is the whole point. It's also what some of my own work has tried to put a number on — valuation changes as implicit transfers across cohorts (“Winners and Losers When Interest Rates Change” , with Dan Greenwald, Matteo Leombroni, and Stijn Van Nieuwerburgh).

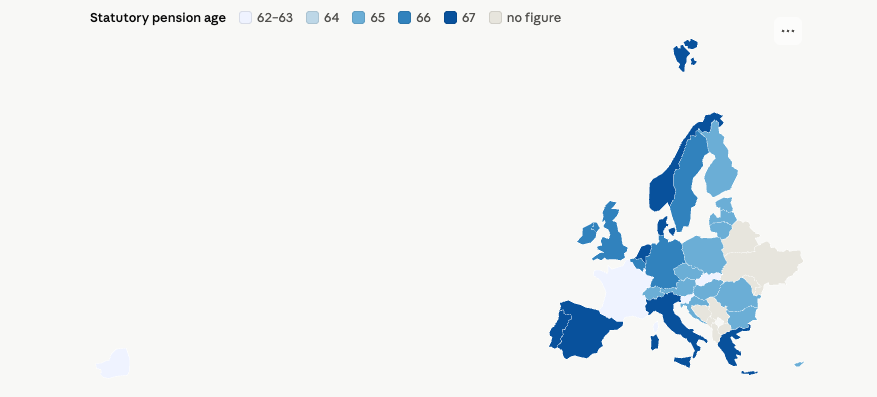

There is a long history of attempts at structural pension reform in France. The most recent example is the 2023 Borne reform which was going to raise the legal retirement age from 62 to 64. France’s legal retirement age is currently at the low end of the European range. Most of its neighbors are at 65, and some are already at 67 including the Nordics, Italy, Greece, Spain, Portugal, and the Netherlands. That white area to the west of Belgium and Germany, that’s France in the picture below.

After Bayrou’s government fell, the new Prime Minister, Lecornu, suspended the Borne reform. What happened after his resignation highlights the key point Bayrou trying to make: everything is being done to protect current generations at the cost of future generations. That’s the generational capital structure that Bayrou was pointing at. The young are at the bottom of the generational capital structure. And they have been misled into believing that accumulating more debt is in their best interests. Prior to Bayrou, there was very little public discussion of these intergenerational transfers in France or in the rest of Europe, for that matter.

It’s not all that surprising. The current political landscape, there is no natural partisan home for a discussion of intergenerational equity. Conflict between the rich and the poor sells politically. Conflict between the young and the old doesn’t. For centuries, the left in Europe has always focused on redistribution from the rich to the poor. And, in fact, there are some on the left who actively resist a discussion of intergenerational transfers because they think that’s a distraction from the real story, which is the age-old conflict between the rich and the poor. Also, both the left and the right depend on the votes of the older generation. They’re the ones who come out to vote, and they obviously have no interest in upsetting them. Junior doesn’t vote.

Of course, these really are only intergenerational transfers if you believe that there is an intertemporal budget constraint for the government. In the 2010s, many economists really believed that there was no intertemporal government budget constraint. Governments could simply roll over the debt and grow out of it, because their funding costs were bound to be low, lower than the growth rate of the economy. That was the whole r < g argument. Blanchard made the careful case for this in 2019 — not that the constraint vanishes, but that carrying debt was far cheaper than the textbooks assumed. The wilder version, further to the left, threw the constraint out entirely: a government that prints its own currency can always pay what it owes. The only real limit is inflation.

Everything changed in 2022 when inflation came back and central banks were forced to start shrinking their balance sheets. Now, in 2026, it’s pretty clear that the government intertemporal budget constraint is real. It’s the reason the French Prime Minister was on television, looking tired and defeated, explaining the virtue of lucidity to his countrymen.

Intergenerational transfers are opaque, abstract, and harder to measure than intra-generational transfers. Economists, like Piketty, have spent a lot of time and resources on measuring inequality between the rich and the poor. They have found a huge audience for their work. But it has been harder to reach an audience for the measurement of intergenerational transfers, in spite of the seminal work by people like Auerbach and Kotlikoff. 1

Four days after his TV interview, Bayrou tried to walk back some of his comments in another interview. He clarified that never meant to single out the boomers. After all, he was a boomer himself. He walked back his statements, even though he didn’t really have much to lose.

The most bizarre thing about European politics this summer has been the debate about the merits of AC units during the heatwave. AC has become a polarizing issue between the left and the right, much like immigration. The left and the right will have bruising fights about AC units, but they’ll stay away from the topic of intergenerational transfers. There really is no political home for people who want to draw attention to intergenerational transfers.

So yes — let's get Grandma and Grandpa an AC unit to survive the heat in Paris. They've earned it. And while we're at it, since we're already talking about what one generation owes another, let's talk about pension reform. Same grandparents. Same kids picking up the tab.

Piketty himself never explores the cohort aspects of his work on income and wealth inequality, which is surprising because there are some important cohort implications. His recent endorsement of degrowth highlights that he has a blind spot when it comes to intergenerational equity. Degrowth would obviously have disastrous implications for future generations, especially when it comes to public finances.

Nothing that an increase in the minimum wage and a wealth tax won't solve...

We are not yet grasping that this is truly unique as intergenerational conflicts go (because sheer demographics). And to hear it from the French, who pretty much called first dibs on every modern revolution ( I count the Paris Commune)...