Central Bank Independence: Lessons from Maastricht

On September 25, 2025, an amicus brief was filed at the Supreme Court in Trump v. Cook (No. 25A312). The signatories: all three living former Fed Chairs (Greenspan, Bernanke, Yellen), five former Treasury Secretaries (Rubin, Summers, Paulson, Geithner, Lew), six former CEA Chairs (Hubbard, Mankiw, Romer, Furman, Rouse, Bernstein), former Fed Governor Dan Tarullo, former Senate Banking Chairman Phil Gramm, and economists Ken Rogoff and John Cochrane. Their argument: Fed governors cannot be removed at will by the President. Take that protection away, the signatories warn, and inflation expectations may become unanchored, and US borrowing costs may rise.

The argument makes a ton of sense. A genuinely independent central bank can stick to its narrow mandate without being forced by politicians to help their government fund deficits. If the Fed sticks to its mandate, then monetary policy is credible: low and stable inflation, anchored expectations, and a Treasury market that doesn’t price in a political-interference premium. Bond investors believe the Fed will hike to fight inflation when needed, instead of easing the Treasury’s borrowing costs. Economists call this monetary dominance.

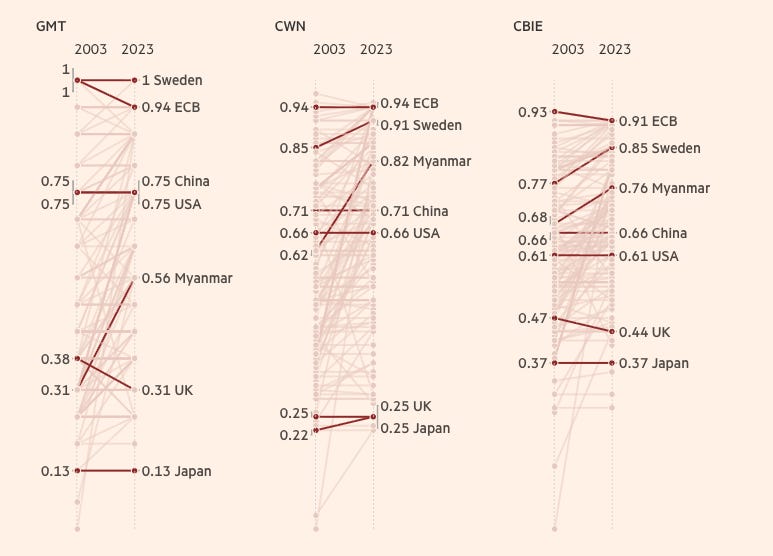

Last Friday, at Hoover’s Annual Monetary Policy conference on Independence, Structure, and Risks Ahead for Central Banks, Luis Garicano (LSE, Silicon Continent) pointed out that central bank independence may not constrain the Fed or other central banks as much as you probably think it does. Exhibit 1 is the European Central Bank. The ECB was designed in 1992 to be more independent than any major central bank in history, with a narrow price stability mandate, a scaled up version of the venerable Bundesbank, in a monetary union explicitly engineered to prevent fiscal experiments. And it worked. The ECB scores very high across three different central bank independence indices constructed by academic economists (for central bank geeks: GMT, CWN and CBIE), much higher than the Fed. If independence-implies-narrow-execution holds anywhere, it should hold for the ECB.

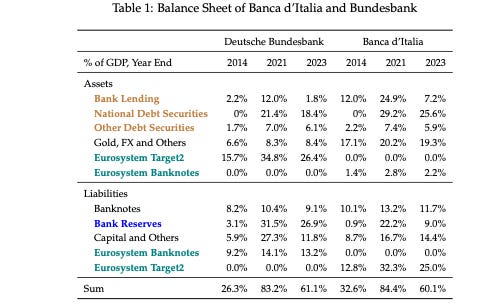

It doesn’t. Over the past fifteen years the ECB has used its balance sheet to repeatedly backstop the bond markets of fiscally weak member states, built up trillion-euro cross-country claims through the Eurosystem payments system, and transferred billions of euros across national taxpayers — none of it approved by any legislators. The Bundesbank saw its balance sheet balloon to 83% of German GDP in 2021. The Banca d’Italia grew its balance sheet to 84% of Italian GDP.

The takeaway isn’t that the amicus signatories are wrong, but even an independent central bank can easily color outside the lines when it wants to, and central bankers are typically not held accountable.

The mandate

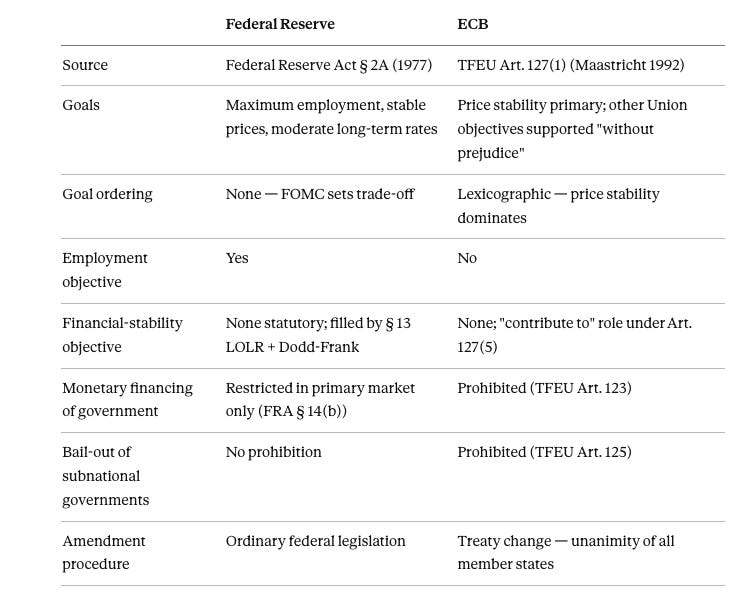

Let’s go over the Fed’s mandate first. Section 2A of the Federal Reserve Act was added by the Federal Reserve Reform Act of 1977:

The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

Three goals — employment, prices, long-term rates — listed without ranking. The “dual mandate” treats moderate long-term rates as derivative; the FOMC reads it that way. The FOMC sets the trade-offs between the goals. When the FOMC chose in 2020 to tolerate above-target inflation in service of a faster employment recovery — “flexible average inflation targeting” — that was a discretionary trade-off entirely within § 2A. The ECB wouldn’t have been allowed to do this.

The ECB was conceived in a charming little town on the Dutch-Belgian border. The Maastricht designers, working from the Delors Report of 1989 with heavy German input, modeled the ECB on the Bundesbank. The Bundesbank had delivered low and stable West German inflation through the 1970s and 1980s while the Fed under Burns and Miller produced the Great Inflation. The narrow mandate was the lesson.

The Maastricht designers built in several layers of protection — a narrow mandate, and a strong independence regime. The ECB’s mandate, Article 127(1) TFEU, looks very different from the Fed’s:

The primary objective of the European System of Central Banks (hereinafter referred to as “the ESCB”) shall be to maintain price stability. Without prejudice to the objective of price stability, the ESCB shall support the general economic policies in the Union with a view to contributing to the achievement of the objectives of the Union as laid down in Article 3 of the Treaty on European Union.

This is quite different from the Fed’s § 2A. First, the objectives are lexicographically ordered. Price stability is primary; everything else — employment, growth, financial stability, the rest of the Article 3 goal list — is supported only “without prejudice” to price stability. There is no trade-off. Second, employment is not even an objective. The Fed could — and did, in 2009 and again in 2020 — justify large-scale balance-sheet operations on the ground that they support employment. The ECB cannot make that argument. A third, less obvious asymmetry sits in Article 127(5):

The ESCB shall contribute to the smooth conduct of policies pursued by the competent authorities relating to the prudential supervision of credit institutions and the stability of the financial system.

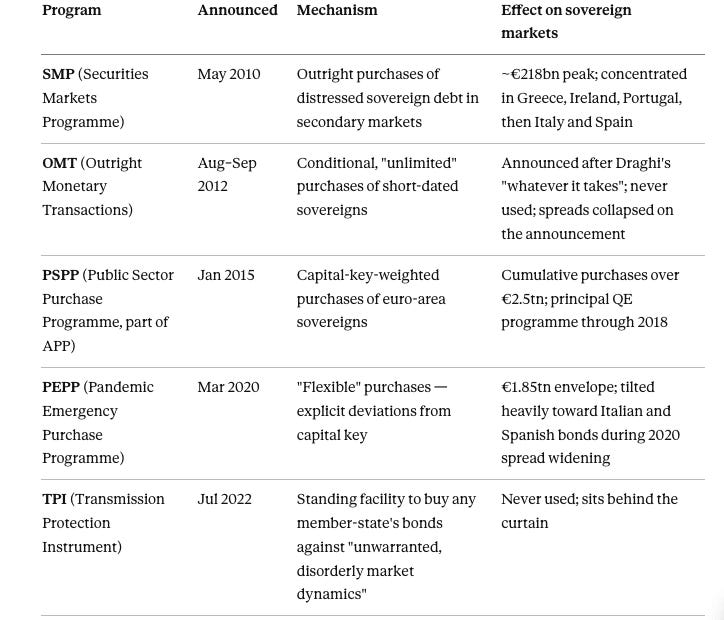

Financial stability is not an objective. The ECB’s financial-stability operations since 2010 — the SMP, OMT, PEPP, the eventual TPI — have all had to be justified as monetary-policy operations.

Then come two prohibitions. Article 123 TFEU forbids monetary financing of governments:

Overdraft facilities or any other type of credit facility with the European Central Bank or with the central banks of the Member States … in favour of Union institutions, bodies, offices or agencies, central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of Member States shall be prohibited, as shall the purchase directly from them by the European Central Bank or national central banks of debt instruments.

Article 125 TFEU is the “no bail-out” clause:

The Union shall not be liable for or assume the commitments of central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of any Member State … A Member State shall not be liable for or assume the commitments of central governments [of] another Member State…

Section 14(b) of the Federal Reserve Act restricts Fed primary-market purchases of Treasuries, but secondary-market purchases — the entire substance of US QE — are unrestricted. Article 123 forecloses direct lending; Article 125 forecloses mutualization.

On paper, this should have constrained the ECB to just focus on fighting inflation without getting dragged into fiscal issues. That’s not what happened.

There is a whole alphabet soup of programs which the ECB has rolled out to support the bond markets of individual member states. Each one was framed as monetary policy. Each of these compressed sovereign spreads at moments when one or more governments would otherwise have faced funding difficulties.

The pattern is pretty obvious. Legal framing: price stability or transmission. Operational trigger: sovereign-spread distress in a periphery country. Institutional safeguard: conditionality — for OMT, an ESM program; for TPI, “compliance with EU fiscal frameworks.” Market impact: compress spreads.

So why is no one holding the ECB accountable for coloring outside of the lines? The German Federal Constitutional Court — the Bundesverfassungsgericht (try saying that twice very fast) or BVerfG, seated in Karlsruhe — has at various points ruled that this is in fact fiscal policy. In its May 5, 2020 PSPP judgment, the BVerfG held that the ECB had failed to demonstrate that PSPP’s “economic policy effects” were proportionate to its monetary-policy aims, and declared that the Bundesbank could not continue participating unless the ECB produced a satisfactory proportionality analysis.

The BVerfG has no direct jurisdiction over the ECB. The judgment was addressed to the Bundestag, the Bundesregierung, and the Bundesbank, instructing them to obtain a satisfactory proportionality analysis within three months, on pain of the Bundesbank withdrawing from PSPP. Within the three-month window, the ECB Governing Council produced (non-public) proportionality documentation on its own terms.

And then the Germans blinked. The Bundestag declared itself satisfied. The Bundesregierung concurred. The BVerfG closed the case on April 29, 2021. The nuclear option — ordering the Bundesbank out of PSPP — was never on the table. Withdrawal could have meant de facto German exit from the Eurosystem. The ECB has proven itself to be the better poker player.1

The BVerfG is, on paper, the strongest available institutional check on the ECB. But that check has proven ineffective because the cost of using it may be a German exit from the euro.

According to the ECB, the laundry list of asset purchase programs neatly fits into its narrow mandate because it must defend the transmission mechanism of monetary policy. If the spread between Italian and German 10-year yields widens by 200 basis points, the argument runs, the same policy rate produces different financing conditions in different member states. The remedy is to compress the spread — mechanically, by buying the bonds of the country whose spread has widened.

Ironically, one of the main reasons credit conditions in the periphery depend on the spread is that the local banks own a significant fraction of their country’s sovereign bonds. During the sovereign debt crisis and its aftermath, the ECB provided cheap funding to these banks in the periphery that was explicitly designed to help them buy their own government’s bonds.

Any sovereign-spread widening can be characterized as a threat to transmission, including widenings driven by poor fiscal choices at home. Once the ECB targets spreads in defense of transmission, it has provided a backstop for national governments. That is fiscal policy — and the narrow mandate does not seem to prevent it.

The July 2022 TPI announcement codified this approach. The TPI permits purchases “to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area.” The operative word is “unwarranted.” The ECB gets to decide in real time whether sovereign spreads are warranted by fundamentals. If you’re a central banker and you know how to do that, you should probably consider moving from Frankfurt to Greenwich, CT, and start a macro hedge fund.

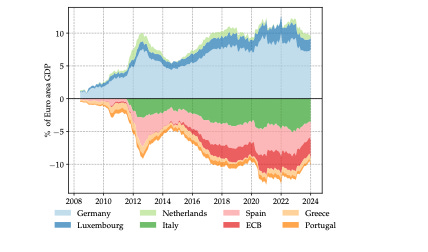

The second channel through which the ECB does fiscal work is the Eurosystem’s internal balance sheet. When the ECB expands its balance sheet, it issues reserves and cash mostly in the core countries. The NCBs in periphery countries then borrow from the core NCBs at below-market rates (through TARGET-2), and use these funds to finance asset purchases and bank lending.2 This arrangement exposes taxpayers in core countries to credit and currency risk without corresponding compensation. In “What does it Take?”, my co-authors Matteo Leombroni (Boston College), Zhengyang Jiang (Kellogg), Yili Chien (St-Louis Fed) and I measured these transfers by comparing the cross-country distribution of NCB income to a counterfactual scenario without non-marketable intra-Eurozone claims.

How big are these transfers? Between 2004 and 2023, Germany paid a cumulative cross-country transfer of 10.9% of GDP to the rest of the Eurosystem. Italy and Spain received cross-country subsidies of 5.7% and 7.5% of their respective GDPs over the same period. These are flows that no parliament voted on.

The ECB was designed to be the most independent central bank with the narrowest mandate that could be written. It didn’t quite work as planned. The mandate itself turned out to be a much weaker constraint than the Eurozone’s founding fathers in 1992 believed. Any country that hopes to use central bank independence to insulate monetary policy from increasing fiscal pressure should study the ECB’s experience. Without real accountability, central bank independence can be positively harmful, as my colleague Amit Seru has pointed out. You may end up with technocrats engineering fiscal transfers without any mandate from voters to do so.

Far from rewarding Germany for trying to hold the ECB accountable, the European Commission even opened Article 258 TFEU infringement proceedings against Germany on June 9, 2021 over the ultra vires declaration. The Commission alleged that the BVerfG’s ultra vires declaration violated fundamental principles of EU law and interfered with the judicial mandate of the Court of Justice of the EU as the final interpreter of EU law.

**TARGET2 imbalances.** The Eurosystem’s real-time gross-settlement system books cross-border euro flows as claims on and liabilities to the Eurosystem. Persistent imbalances accumulate. By mid-2022, the Bundesbank was a net creditor of roughly **€1.16 trillion**; Banca d’Italia a net debtor of roughly **€650 billion**; Banco de España of roughly **€500 billion**. These claims earn (or pay) the deposit-facility rate inside the Eurosystem.

In a fiscal union, TARGET2 imbalances would have no national interpretation — they’d be internal Fed balance-sheet entries. In the Eurosystem, where each NCB consolidates with a specific national taxpayer, they have a very direct national interpretation.

Very interesting post as always!

Trying to rephrase one of your core arguments:

Central bank independence is not enough to ensure a narrow interpretation of the mandate. To ensure this, central banks need to be held accountable.

But how?

In a democracy with checks and balances, the judicial branch seems like an obvious choice. You also write: “The BVerG is, on paper, the strongest available institutional check on the ECB.” But why isn’t it the European court of justice?

Interesting analysis, thanks. I think it highlights the limitations of pursuing any goal other than stability of a currency union when you’re the central bank of a currency union. Not sure it goes through to the case of other central banks that have their own currency and a floating exchange rate.